ETF 105: Gain Efficient Access to Bond Markets With Fixed Income ETFs

September 27, 2019

Read Time 10 MIN

ETF 101: Understanding the Basics

ETF 102: The Inner Workings of ETF Creations and Redemptions

ETF 103: Is This ETF Right for Your Portfolio?

ETF 104: Getting the Most Out of Your ETF Trades

ETF 105: Gain Efficient Access to Bond Markets with Fixed Income ETFs

ETF 106: Debunking Fixed Income Myths

ETF 107: Passive vs. Active ETFs Explained

Trading bonds vs. Equities

While equities typically trade on centralized exchanges where buyers and sellers are able to observe transactions and obtain executable quotes, bonds are generally traded OTC, with buyers and sellers negotiating prices directly with one another. This means they have less transparency into prices that other market participants have transacted at. Most bonds also trade infrequently, or not at all, throughout the day, making it difficult to estimate the fair price of a bond. Unlike stocks, which can be traded in single share increments, bonds typically trade in minimum amounts that can sometimes be tens or even hundreds of thousands of dollars.

These characteristics reflect the institutional nature of the bond market, where large investors with sophisticated trading and research capabilities dominate the market. This can make it difficult and expensive for individual investors to invest directly in these markets and build diversified portfolios.

Ease of Access via ETFs

Since the first fixed income ETFs were launched in 2002, the space has increased significantly in size, number of funds, and the diversity of strategies available as adoption has grown and investors have become more familiar with the benefits they may provide. Previously, given the difficulty in buying the underlying bonds, individual investors seeking diversified exposure typically had to access these markets through actively managed mutual funds. In addition to the generally higher cost of these strategies, achieving targeted exposures can be more difficult because of the lack of transparency and the fact that managers have flexibility to invest in securities outside of their benchmark in order to generate alpha. However, studies have shown that the majority of active managers have underperformed the broad market benchmark, providing further demand for low-cost passive strategies in the ETF wrapper.

Investors can now find ETFs that provide access to broad segments of the market, including “core” aggregate exposures as well as specific sectors such as corporate, government, and municipal bonds. Further, areas that were once difficult or expensive to access can now be accessed through single trades, including emerging markets bonds, high yield municipal bonds and bank loans. In addition to accessing broad segments of the market, ETFs also provide the ability to target specific exposures within each sector, for example by applying screens based on geography, maturity, credit quality.

The large variety of offerings has made it easier for investors to efficiently build tailored portfolios based on their investment objectives and risk profiles.

Fixed Income ETF Myths vs. Reality:

Fixed income ETF investors do not know what they are buying.

Most sponsors will provide portfolio holdings through a variety of mediums (i.e., fund’s webpage, Bloomberg, third-party data vendors, etc.). Unlike mutual funds (which will typically display holdings on a 30-60-day lag), most passive ETFs will display holdings on a one day lag at the latest.

There is a discrepancy between the “promised” liquidity of fixed income ETFs and the liquidity of the underlying securities.

Bonds inherently are less liquid for a number of reasons. All bonds are traded over-the-counter, so there is no centralized exchange like there is for equites. Bonds trade by “appointment,” meaning the two counterparties must find each other and then negotiate terms of the trade. As a result in some instances bonds can go for days, weeks, or even months without trading. Although the liquidity of its underlying securities is an important component of any ETF’s overall liquidity profile, it is just a segment of the fund’s overall liquidity. In many instances, we see ETF trading occur without a single primary market transaction occurring, meaning there are no direct transactions in the ETF’s underlying bonds directly as a result of an ETF transaction on the secondary market, or an exchange. Less than 50% of fixed income ETF trading volume in the secondary market leads directly to primary market trades in its underlying securities.

It is also worth noting that ETFs are merely a liquidity vehicle that distributes costs differently than their sister vehicles, mutual funds. One of the main differentiating factors of ETFs vs. mutual funds is the fact that ETFs trade on exchange and that each transaction may or may not trigger primary market activity. Mutual fund investors create and redeem at NAV and in the case of redemptions, the costs are borne by the remaining investors. Investors in ETFs sell in the secondary market (only authorized participants can transact in the primary market) at a cost dictated by the market maker and ultimately borne by the selling investor. (See ETF 102: The Inner Workings of ETF Creation and Redemption for more on primary and secondary markets and the role of authorized participants.)

During periods of market sell-offs, investors will become forced sellers of ETFs, liquidity will diminish, and secondary market spreads will widen.

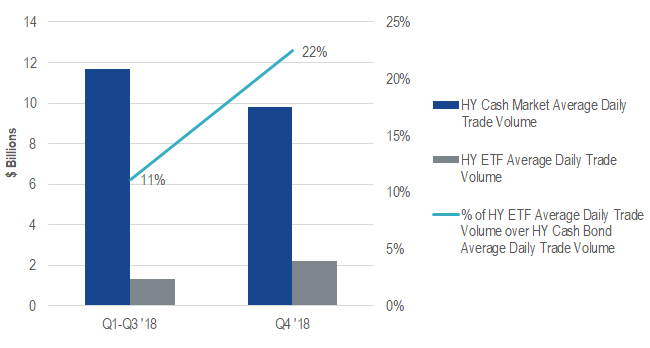

Fixed income ETFs actually experienced enhanced liquidity amidst periods of heightened volatility, such as in the fourth quarter of 2018. We analyzed high yield (HY) fixed income ETFs trading volume below.

HY Cash Bond Market Average Daily Trade Volume[1]

- Q1 – Q3 2018: $1.3B

- Q4 2018: $9.8B

HY Fixed Income ETF Average Daily Trade Volume

- Q1 – Q3 2018: $11.7B

- Q4 2018: $2.2B

High Yield Average Daily Trade Volume

Source: Bloomberg, SIFMA.

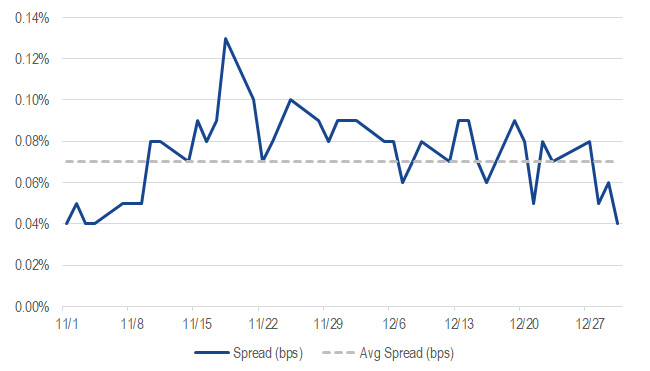

We actually saw fixed income HY ETF trading double from 11% to 22% as a percentage of HY cash bond trading when comparing activity during Q1-Q3 versus activity in Q4, and the average daily trade volume of high yield ETF surging almost 70%, from $1.3B to $2.2B, in the fourth quarter of last year alone. In addition, in terms of spreads, in the case of VanEck® Fallen Angel High Yield Bond ETF (ANGL®), we saw spreads on exchanges marginally tighten when comparing average volume-weighted bid-ask spreads of Q1-Q3 (7 bps) to Q4 (6 bps). In other words, the increased liquidity in the ETF resulted in lower trading costs to investors during this volatile period.

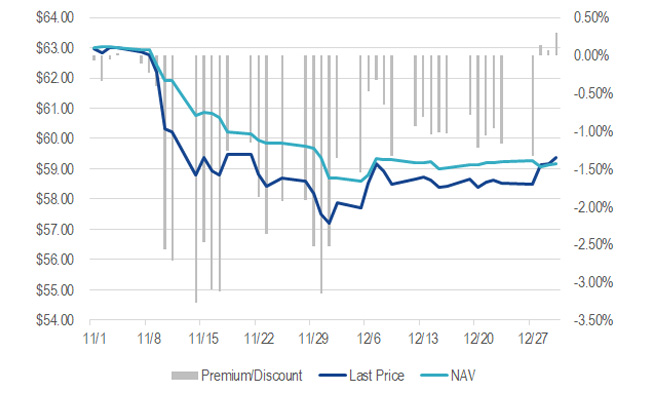

The fact that fixed income ETFs may experience large premiums and discounts are a testament to their lack of liquidity.

Pronounced premiums or discounts do not necessarily mean the ETF’s secondary market price is mispriced—rather, the ETF’s secondary market price may be acting as a price discovery vehicle for its underlying portfolio of bonds. ETF sponsors will generally rely on a third-party pricing provider to calculate NAV. However, even these third-party pricing providers run into issues with accuracy around pricing bonds that not only trade OTC, but may not have traded for a period of time.

During periods of extreme market volatility, one may experience a pronounced discount, trading in excess of the fund’s average daily volume as well as outflows. For example, take a look at VanEck®High-Yield Municipal Index ETF’s (HYD®) activity during the 2016 election

Daily Average Volume-Weighted Spreads

High Yield Municipal Index ETF (HYD): Premium/Discounts

Source: NYSE Arcavision, Bloomberg, VanEck.

For HY munis, a subset of the portfolio typically won’t trade for days, weeks, or months in some instances. During a period of market duress and heightened volatility, the ETF may trade at a discount while it waits for NAV to “catch-up” to valuations that are more in line with the market. NAVs are dictated by a third-party pricing provider, and their pricing may lag behind the true value of those bonds if they were to actually trade. Note, however, the relatively quick “snapback” following periods of time when the discount exceeded 2-3%.

Tapping into ETF Liquidity

In addition to providing targeted access to the bond market, investors may also benefit from the liquidity that ETFs provide. Investors can use ETFs to add or reduce exposures in a way that can potentially minimize friction costs. The liquidity of many fixed income ETFs, particularly larger ETFs, may often be greater than the underlying bonds they hold. In other words, the ETF wrapper provides a layer of secondary market liquidity that is additive to what can be found in the primary market. This is because a transaction in an ETF does not necessarily require trades in the underlying bonds. For example, ETF orders between buyers and sellers may be matched on the stock exchange. This additional layer of liquidity may result in lower trading costs, as measured by bid-ask spreads.

Ultimately, however, liquidity is driven by the fund’s underlying holdings, which helps to create a lower bound on the liquidity of the ETF shares themselves.

It is therefore important for index providers to design indices that emphasize the liquidity of the constituents. In addition, bond ETF portfolio managers engage in techniques such as optimization—holding a subset of the securities in an index that are considered representative of the risk and return exposures of the full index—which minimizes transaction costs and helps to enhance ETF liquidity. This results in potentially lower bid-ask spreads for investors when trading the ETF on an exchange.

Liquidity is a defining feature of ETFs, and is particularly appealing for fixed income ETFs given the less liquid nature of the underlying bond market. Further, with bond trading desks holding less inventory for market-making purposes as a result of higher capital requirements following post-financial crisis regulation, this feature has become increasingly important.

Unlocking Transparency of Fixed Income ETFs

Another benefit of using ETFs for fixed income exposure is the transparency provided, both in terms of pricing, holdings, and cost of ownership. As mentioned above, their exchange-traded nature allows investors to see real-time transactions and quoted bids and offers, unlike what is found in the bond markets themselves. Investors know the current value of their holdings and have a good indication of where they could buy or sell shares. This pricing transparency of fixed income ETFs has provided a benefit to the broader fixed income market, as the ETF prices become better reflections of real-time value than the valuations and last traded prices on the underlying securities.

Like other ETFs, portfolio holdings are disclosed daily on ETF provider websites, along with other descriptive information on risk characteristics and exposures. Investors can see security level detail and know what bonds their ETF holds, which is generally not possible when using mutual funds for fixed income exposure, as they typically only disclose holdings monthly or quarterly, and often with a time lag.

The cost of ownership is also arguably more transparent than other ways of accessing the bond market. The observable quotes provide an indication of where trades can be executed for a given size, and thoughtful trading strategies may provide investors with more pricing certainty and limit the risk of poor execution. Further, costs associated with ETF inflows, outflows, and portfolio trading are borne by the shareholders engaged in the transactions, rather than existing investors. This results in a more equitable distribution of costs, in which the transacting investors who create trading costs or demand immediate liquidity bear those costs. (See ETF 103: Is This ETF Right for You? for more on ETF cost of ownership.)

Key Takeaways: Fixed Income ETF Flexibility

Fixed income ETFs provide a degree of flexibility for investors that is not typical in the bond markets. The low cost, transparent, and diversified nature of ETFs have broad appeal to investors seeking a strategic long-term holding, while the additional layer of liquidity provided by ETFs can benefit more tactical investors. Because they trade on an exchange like a stock, they also provide investors with the ability to buy shares on margin or take short positions.

Related Insights

Follow Us

IMPORTANT DISCLOSURES

1 Average daily trade volume is the average number of shares of a given security traded within a day over a certain period of time.

This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results, are valid as of the date of this communication and subject to change without notice. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

An investment in the VanEck® Fallen Angel High Yield Bond ETF (ANGL®) may be subject to risk which includes, among others, high yield securities, foreign securities, foreign currency, credit, interest rate, restricted securities, market, operational, call, sampling, basic materials, energy, financial services, telecommunications, index tracking, authorized participant concentration, no guarantee of active trading market, trading issues, passive management, fund shares trading, premium/discount and liquidity of fund shares and concentration risks, all of which may adversely affect the Fund.

An investment in the VanEck®High-Yield Municipal Index ETF’s (HYD®) may be subject to risks which include, among others, municipal securities, high yield securities, credit, interest rate, call, private activity bonds, health care bond, industrial development bond, tobacco bond, California, Illinois, market, operational, sampling, index tracking, tax, authorized participant concentration, no guarantee of active trading market, trading issues, passive management, fund shares trading, premium/discount and liquidity of fund shares and concentration risks, all of which may adversely affect the Fund. High-yield municipal bonds are subject to greater risk of loss of income and principal than higher-rated securities, and are likely to be more sensitive to adverse economic changes or individual municipal developments than those of higher-rated securities. Municipal bonds may be less liquid than taxable bonds. A portion of the dividends you receive may be subject to the federal alternative minimum tax (AMT).There is no guarantee that the Fund’s income will be exempt from federal, state or local income taxes, and changes in those tax rates or in alternative minimum tax rates or in the tax treatment of municipal bonds may make them less attractive as investments and cause them to lose value. Capital gains, if any, are subject to capital gains tax.

The "Net Asset Value" (NAV) of a VanEck Exchange Traded Fund (ETF) is determined at the close of each business day, and represents the dollar value of one share of the fund; it is calculated by taking the total assets of the fund, subtracting total liabilities, and dividing by the total number of shares outstanding. The NAV is not necessarily the same as the ETF's intraday trading value. VanEck ETF investors should not expect to buy or sell shares at NAV.

ETF Fund shares are not individually redeemable and will be issued and redeemed at their NAV only through certain authorized broker-dealers in large, specified blocks of shares called “creation units” and otherwise can be bought and sold only through exchange trading. Shares may trade at a premium or discount to their NAV in the secondary market. You will incur brokerage expenses when trading Fund shares in the secondary market. Past performance is no guarantee of future results. Returns for actual Fund investments may differ from what is shown because of differences in timing, the amount invested, and fees and expenses.

Diversification does not assure profit nor protect against loss.

Investing involves risk, including possible loss of principal. Bonds and bond funds will decrease in value as interest rates rise. An investor should consider investment objectives, risks, charges and expenses of the Fund carefully before investing. To obtain a prospectus and summary prospectus, which contains this and other information, call 800.826.2333 or visit vaneck.com. Please read the prospectus and summary prospectus carefully before investing.

Related Insights

March 23, 2020

Execute ETF trades as cost efficiently as possible by sticking to these important trading best practices.

September 13, 2019

September 03, 2019

The creation and redemption process is a fundamental feature of the ETF structure. Learn how this process works and its role in driving liquidity and tax efficiency for investors.

August 15, 2019

August 05, 2019

Related Funds

IMPORTANT DISCLOSURES

1 Average daily trade volume is the average number of shares of a given security traded within a day over a certain period of time.

This is not an offer to buy or sell, or a solicitation of any offer to buy or sell any of the securities mentioned herein. The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results, are valid as of the date of this communication and subject to change without notice. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

An investment in the VanEck® Fallen Angel High Yield Bond ETF (ANGL®) may be subject to risk which includes, among others, high yield securities, foreign securities, foreign currency, credit, interest rate, restricted securities, market, operational, call, sampling, basic materials, energy, financial services, telecommunications, index tracking, authorized participant concentration, no guarantee of active trading market, trading issues, passive management, fund shares trading, premium/discount and liquidity of fund shares and concentration risks, all of which may adversely affect the Fund.

An investment in the VanEck®High-Yield Municipal Index ETF’s (HYD®) may be subject to risks which include, among others, municipal securities, high yield securities, credit, interest rate, call, private activity bonds, health care bond, industrial development bond, tobacco bond, California, Illinois, market, operational, sampling, index tracking, tax, authorized participant concentration, no guarantee of active trading market, trading issues, passive management, fund shares trading, premium/discount and liquidity of fund shares and concentration risks, all of which may adversely affect the Fund. High-yield municipal bonds are subject to greater risk of loss of income and principal than higher-rated securities, and are likely to be more sensitive to adverse economic changes or individual municipal developments than those of higher-rated securities. Municipal bonds may be less liquid than taxable bonds. A portion of the dividends you receive may be subject to the federal alternative minimum tax (AMT).There is no guarantee that the Fund’s income will be exempt from federal, state or local income taxes, and changes in those tax rates or in alternative minimum tax rates or in the tax treatment of municipal bonds may make them less attractive as investments and cause them to lose value. Capital gains, if any, are subject to capital gains tax.

The "Net Asset Value" (NAV) of a VanEck Exchange Traded Fund (ETF) is determined at the close of each business day, and represents the dollar value of one share of the fund; it is calculated by taking the total assets of the fund, subtracting total liabilities, and dividing by the total number of shares outstanding. The NAV is not necessarily the same as the ETF's intraday trading value. VanEck ETF investors should not expect to buy or sell shares at NAV.

ETF Fund shares are not individually redeemable and will be issued and redeemed at their NAV only through certain authorized broker-dealers in large, specified blocks of shares called “creation units” and otherwise can be bought and sold only through exchange trading. Shares may trade at a premium or discount to their NAV in the secondary market. You will incur brokerage expenses when trading Fund shares in the secondary market. Past performance is no guarantee of future results. Returns for actual Fund investments may differ from what is shown because of differences in timing, the amount invested, and fees and expenses.

Diversification does not assure profit nor protect against loss.

Investing involves risk, including possible loss of principal. Bonds and bond funds will decrease in value as interest rates rise. An investor should consider investment objectives, risks, charges and expenses of the Fund carefully before investing. To obtain a prospectus and summary prospectus, which contains this and other information, call 800.826.2333 or visit vaneck.com. Please read the prospectus and summary prospectus carefully before investing.

Related Insights

March 23, 2020

Execute ETF trades as cost efficiently as possible by sticking to these important trading best practices.

September 13, 2019

September 03, 2019

The creation and redemption process is a fundamental feature of the ETF structure. Learn how this process works and its role in driving liquidity and tax efficiency for investors.

August 15, 2019

August 05, 2019